The Bell Curve of Telematics Adoption: Why Standing Still Means Falling Behind

The window for "early adoption" of telematics in commercial auto insurance has already closed. Here's where the industry stands today, and why indecision is no longer neutral — it's regression.

A perspective on where the commercial auto insurance industry stands today, and why the window for "early adoption" has already closed.

Every Innovation Follows the Same Path

In every industry, new technology follows a predictable pattern of adoption. Everett Rogers described it decades ago, and it has held true for everything from the telephone to cloud computing: a small group of innovators takes the leap first, followed by early adopters, then the early majority, the late majority, and finally the laggards. This is the technology adoption bell curve, and it is as reliable as gravity.

Telematics in commercial auto insurance is no exception.

What began as a niche capability — a handful of forward-thinking carriers experimenting with ELD data for underwriting — has matured into an industry-defining capability. Today, telematics-driven safety scores, risk analytics, and real-time fleet visibility are no longer optional features. They are the foundation of competitive underwriting. The early movers understood this. They invested in aggregation platforms, built workflows around telematics data, and began making better underwriting decisions while their competitors were still debating whether telematics was worth the effort.

The bell curve of telematics adoption in commercial auto insurance is not hypothetical. It is happening right now. And the question every carrier, MGA, and RRG should be asking is: Where am I on this curve?

We Are Approaching the Top, Not the Beginning

Here is the uncomfortable truth that many in the industry have not yet internalized: the adoption of advanced telematics in commercial auto insurance is not in its early stages. It is rapidly approaching the peak of the bell curve.

TruckerCloud now aggregates data from over 170 ELD and telematics service providers, delivering safety scores and analytics to a growing network of carriers, MGAs, and RRGs. The platform has moved well beyond proof-of-concept. It is embedded in underwriting workflows, pre-bind and post-bind risk assessment processes, and carrier onboarding pipelines across the industry. The innovators and early adopters did their work. The early majority is deeply engaged. We are approaching the peak of the curve, and once we cross it, the window for competitive adoption begins to close rapidly.

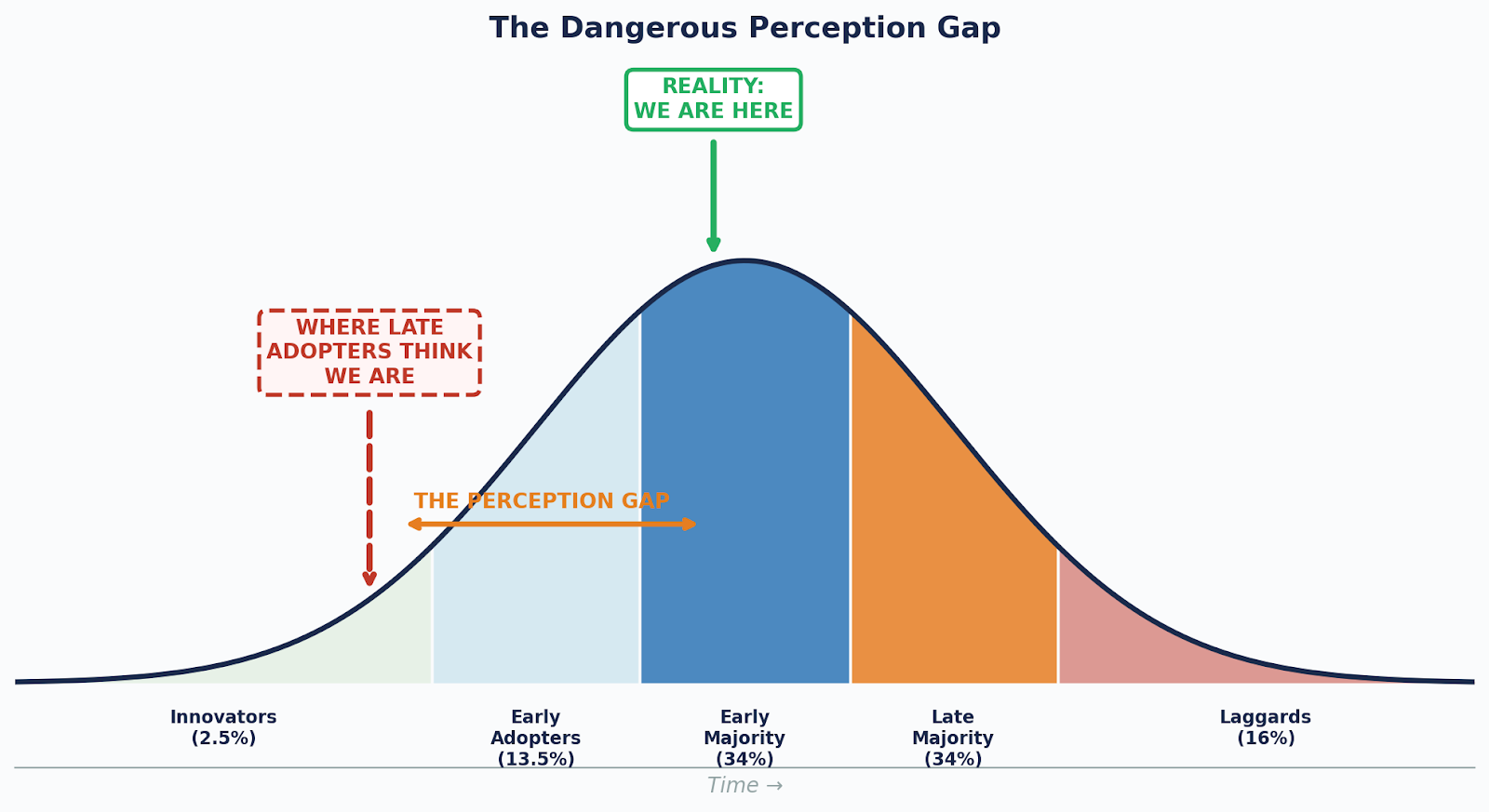

And yet, there is a dangerous perception gap.

Organizations that have not yet adopted advanced telematics tend to believe that they are still in the early stages of the curve — that there is plenty of time to evaluate, pilot, and eventually roll out a telematics strategy. This is a common misconception. It is perhaps the most costly misconception in commercial auto insurance today.

The belief that "we still have time" is rooted in a misunderstanding of where the industry actually stands. The carriers and MGAs who are already leveraging telematics data are not waiting for the rest of the market to catch up. They are compounding their advantage every quarter: refining their models, deepening their data sets, and widening the gap between themselves and everyone else.

The chart above illustrates the core problem: late adopters believe the industry is still in the early-adopter phase, when in reality, adoption is approaching the peak. This gap between perception and reality is where competitive disadvantage takes root.

Past the Peak: Indecision Is Not Neutrality. It Is Regression.

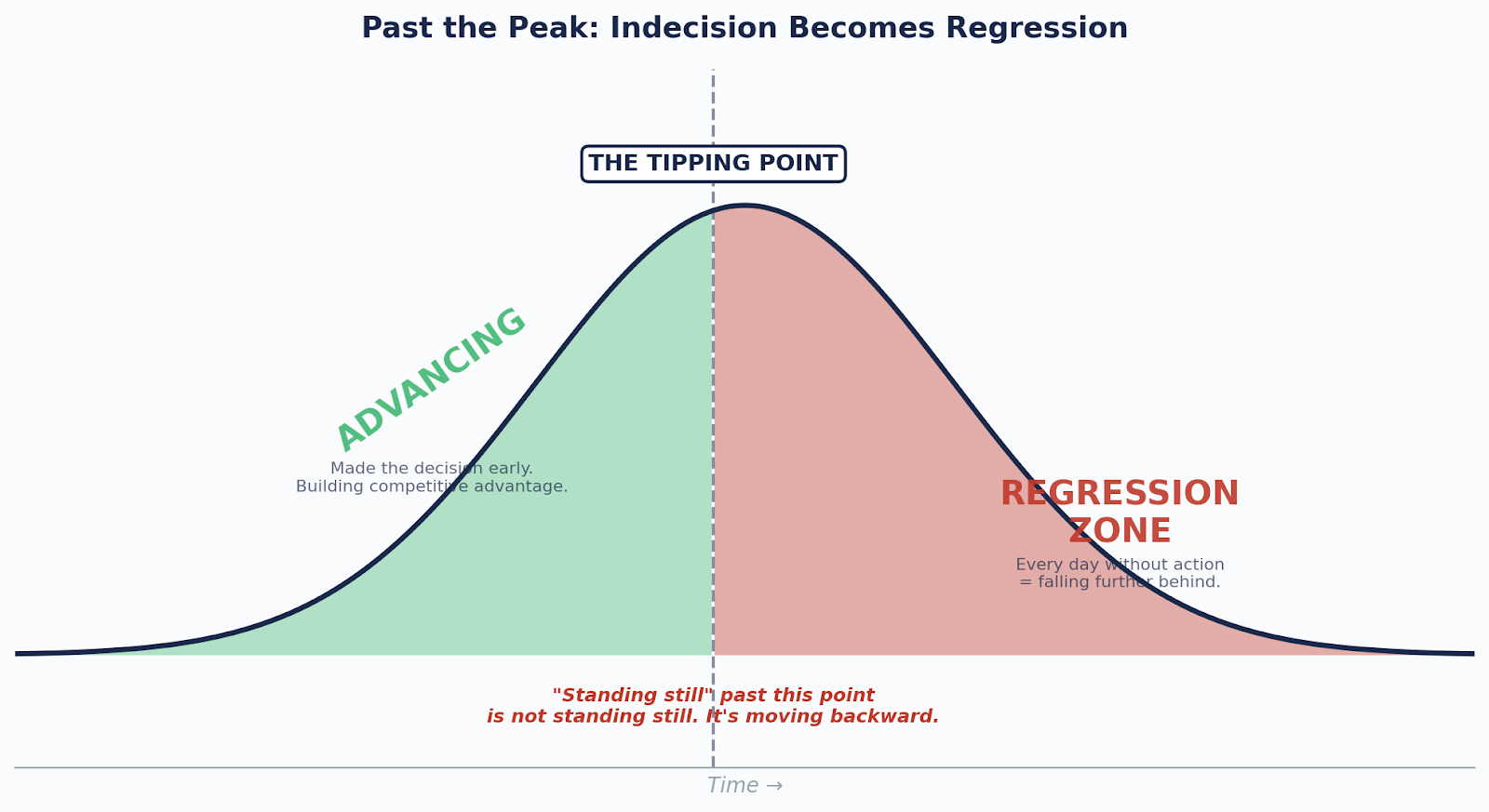

There is a critical misunderstanding that pervades organizations that have delayed telematics adoption: the belief that by not making a decision, they are maintaining the status quo. They are not. They are regressing.

In a static market, standing still is standing still. But commercial auto insurance is not a static market. It is a market in motion, one where the competitive baseline is rising every month. When your competitors are using telematics data to price risk more accurately, identify unsafe fleets before losses occur, and retain the best-performing accounts, your lack of the same capability does not leave you where you were. It puts you behind where you were.

Consider the math. If the average underwriting accuracy in your segment improves by even a few percentage points each year due to telematics adoption among your competitors, your book of business is not just failing to improve — it is deteriorating on a relative basis. You are being adversely selected against. The risks your competitors can now see and avoid are the risks that end up in your portfolio. You are not standing still. You are absorbing the risk that smarter underwriting is shedding.

The graphic above draws the line clearly. Before the tipping point, organizations that adopt are advancing: building data assets, training teams, and improving results. After the tipping point, organizations that have not adopted are no longer "not yet started." They are actively falling behind a market that has moved on without them. We are just short of that tipping point right now, which means the time to act is not next quarter. It is today.

Every quarter of delay compounds the problem. The data advantage widens. The talent gap deepens. The cost of catching up increases. What could have been a manageable onboarding process today becomes a crisis remediation effort two years from now.

The Question You Should Be Asking

This article is not a sales pitch. It is a challenge.

If you are a carrier, MGA, or RRG operating in commercial auto insurance, the question is not whether telematics will matter to your business. That question has been answered. The question is: Where are you on the curve, and where do you want to be?

If you adopted early, you are already building on a foundation that your competitors are only beginning to lay. Your advantage is compounding. Your job is to keep pushing.

If you are in the early majority, you are in the right place at the right time. The tools, integrations, and workflows are mature. The risk of adoption is low, and the cost of inaction is rising. Now is the moment to move decisively.

If you have not yet started — if you are still evaluating, still forming committees, still waiting for the "perfect" time to begin — understand this: the perfect time was two years ago. The next best time is today. Every day you wait, the curve moves on without you, and the distance you need to cover to catch up grows.

The Curve Does Not Wait

The bell curve of technology adoption is not a theory. It is a map of how industries evolve. It has played out in every sector, with every transformative technology, without exception. Telematics in commercial auto insurance is following the same trajectory, and the evidence is now overwhelming.

TruckerCloud's position at the center of this transformation — aggregating data from 170+ telematics providers, serving carriers across the commercial auto landscape — gives us a unique vantage point. We see where the industry is headed because we are helping build the infrastructure that is taking it there.

The curve is approaching its peak. The early majority has moved. The window for adoption before the tipping point is still open, but it will not stay open much longer.

The only question left is yours: Will you ride the curve, or will it leave you behind?

Tiana Schowe, CPCU

Head of Commercial Strategy

TruckerCloud

tiana@truckercloud.com